Quick answer

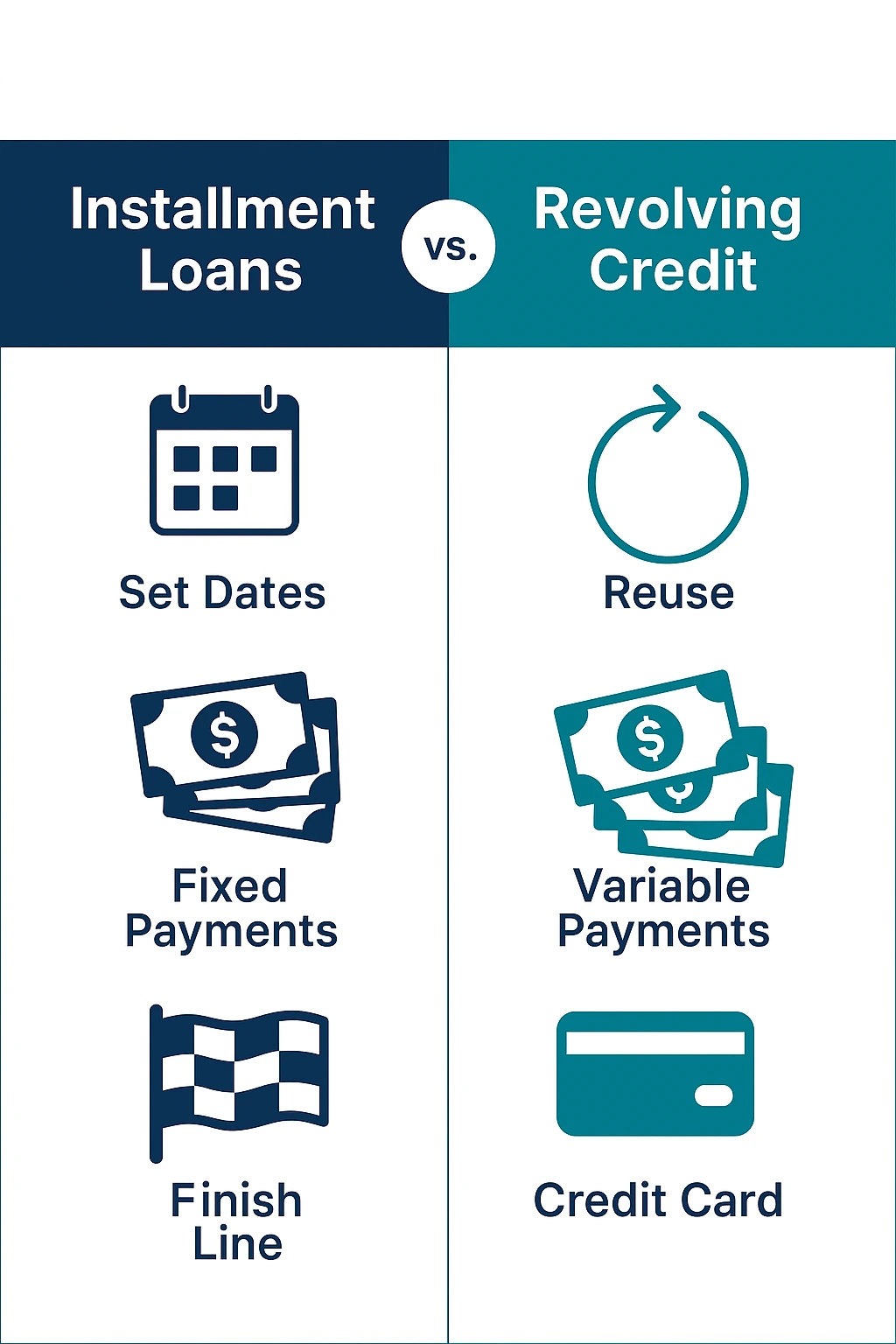

Installment credit is fixed. Revolving credit is reusable.

An installment loan gives you one lump sum that you repay through scheduled payments over a set term.

Revolving credit gives you a credit limit you can borrow from, repay, and use again.

Best for one-time expenses when you want a clear payment amount and payoff timeline.

Best for ongoing access to funds, but balances can grow if you rely on minimum payments.

Neither option is automatically better. The right choice depends on how much you need, how quickly you can repay it, the total cost, and whether the loan or credit line fits your budget.

When you compare installment loans vs. revolving credit, the biggest difference is how the money is borrowed and repaid. Installment credit is built around a fixed loan amount and scheduled payments. Revolving credit is built around access to an open credit line.

This guide breaks down both options in plain language so you can compare repayment structure, interest, credit impact, risks, and common use cases before you borrow.

Installment Credit and Revolving Credit: The Core Difference

Installment credit starts with a set loan amount. You receive the funds once, then repay the balance through scheduled payments. Revolving credit starts with a credit limit. You can use part of that limit, repay it, and borrow again as long as the account stays open and in good standing.

Installment credit

A borrower receives a lump sum upfront and repays it over a defined term. Mortgages, auto loans, student loans, personal loans, and some title loans are common examples.

Revolving credit

A borrower gets access to a credit line and can borrow against it more than once. Credit cards, home equity lines of credit, business lines of credit, and personal lines of credit are common examples.

What Are Installment Loans?

Installment loans provide a lump sum of money upfront that you pay back in regular payments over a set period. The payment schedule is usually defined before you sign, which makes this type of loan easier to budget for than credit with changing balances.

Common Types of Installment Loans

- Car title loans

- Personal loans from banks or credit unions

- Mortgages for home purchases

- Student loans for education expenses

- Auto loans from dealerships

How Installment Loans Work

With an installment loan, you receive the money once. Your payment amount and payoff timeline are usually set when the loan begins. That structure can help when you need a specific amount for a repair, bill, medical expense, or other one-time cost.

For example, a car title loan may be structured as an installment loan when the borrower uses a paid-off vehicle title as collateral, receives funds upfront, and repays the loan through scheduled payments. Freedom Title Loans serves local borrowers through its Boise and Nampa branches, but this article is meant to explain the broader credit comparison.

What Is Revolving Credit?

Revolving credit gives you access to a credit line that can be used, paid down, and used again. Credit cards are the most common example. You have a spending limit, and your available credit changes as you make purchases and payments.

Common Types of Revolving Credit

- Credit cards

- Home equity lines of credit, often called HELOCs

- Business lines of credit

- Personal lines of credit

How Revolving Credit Works

Your monthly payment changes based on your balance, rate, and account terms. If you have a $5,000 credit card limit and use $2,000, your available credit drops until you pay part of the balance back. Interest is usually charged on the outstanding balance when the balance is not paid in full by the due date.

The Federal Reserve Consumer Credit report tracks revolving and nonrevolving credit trends over time. Those categories are useful because they show how differently credit lines and fixed-term loans work in the broader lending market.

Quick Comparison: Installment Loans vs. Revolving Credit

| Feature | Installment Loans | Revolving Credit |

| How funds are received | One lump sum upfront | Access to a reusable credit limit |

| Payment amount | Usually fixed or scheduled | Changes based on balance and terms |

| Payoff timeline | Set term or expected payoff date | No set payoff date if the balance stays open |

| Interest | Often built into the scheduled payment | Often charged on the outstanding balance |

| Access to more money | A new loan is usually required | Available credit can be reused after repayment |

| Common examples | Auto loans, personal loans, mortgages, title loans | Credit cards, HELOCs, personal lines of credit |

| Often best for | One-time expenses with a defined amount | Ongoing or changing expenses |

Click image to view full size

How Interest and Payments Usually Differ

The repayment structure matters because it affects how predictable the debt feels month to month. Installment loans are usually built around a payment plan. Revolving credit is built around an open balance that can change as you use and repay the account.

Installment loan payments

Installment loans usually have a defined loan amount, scheduled payment dates, and a set repayment period. That can make budgeting easier because the borrower can see the expected payoff path before agreeing to the loan.

Revolving credit payments

Revolving credit payments depend on how much of the credit line is used. Paying only the minimum can lower the short-term payment, but it can also keep the balance open longer and increase the total interest paid.

- Is the rate fixed or variable?

- What is the full repayment schedule?

- Are there origination, late payment, or early payoff fees?

- What happens if a payment is missed?

- Is the account reported to credit bureaus?

Pros and Cons of Installment Loans

Possible benefits

- Predictable payment structure

- Set loan amount

- Clearer payoff timeline

- Useful for one-time expenses

- Can be easier to plan around a monthly budget

Possible drawbacks

- Less flexible than a reusable credit line

- A new loan may be required if more funds are needed later

- Some lenders may charge fees or penalties

- Collateral may be required for secured installment loans

- Missed payments can create added cost or risk

Pros and Cons of Revolving Credit

Possible benefits

- Flexible access to funds

- Can be reused as the balance is paid down

- Useful for ongoing or changing expenses

- Interest is generally based on the amount used

- Can help build credit when managed responsibly

Possible drawbacks

- Payment amount can change

- No fixed payoff date if a balance is carried

- Minimum payments can keep debt open longer

- High utilization can hurt credit scores

- Easy access can make overspending more tempting

How Each Option Can Affect Credit

Credit impact depends on the lender, the account type, and whether payments are reported to credit bureaus. For traditional credit products, installment loans and revolving credit are often evaluated differently.

Installment credit impact

Installment loans are usually tied to payment history, remaining balance, loan age, and account status. On-time payments can support a positive credit profile when the lender reports them. Missed payments can have the opposite effect.

Revolving credit impact

Revolving credit often affects credit through utilization, which compares the balance to the credit limit. A high balance compared with the limit can put pressure on credit scores, even when payments are made on time.

Reporting practices vary. Before signing any loan or credit agreement, ask whether the account is reported, when it is reported, and what happens if the account becomes late or past due.

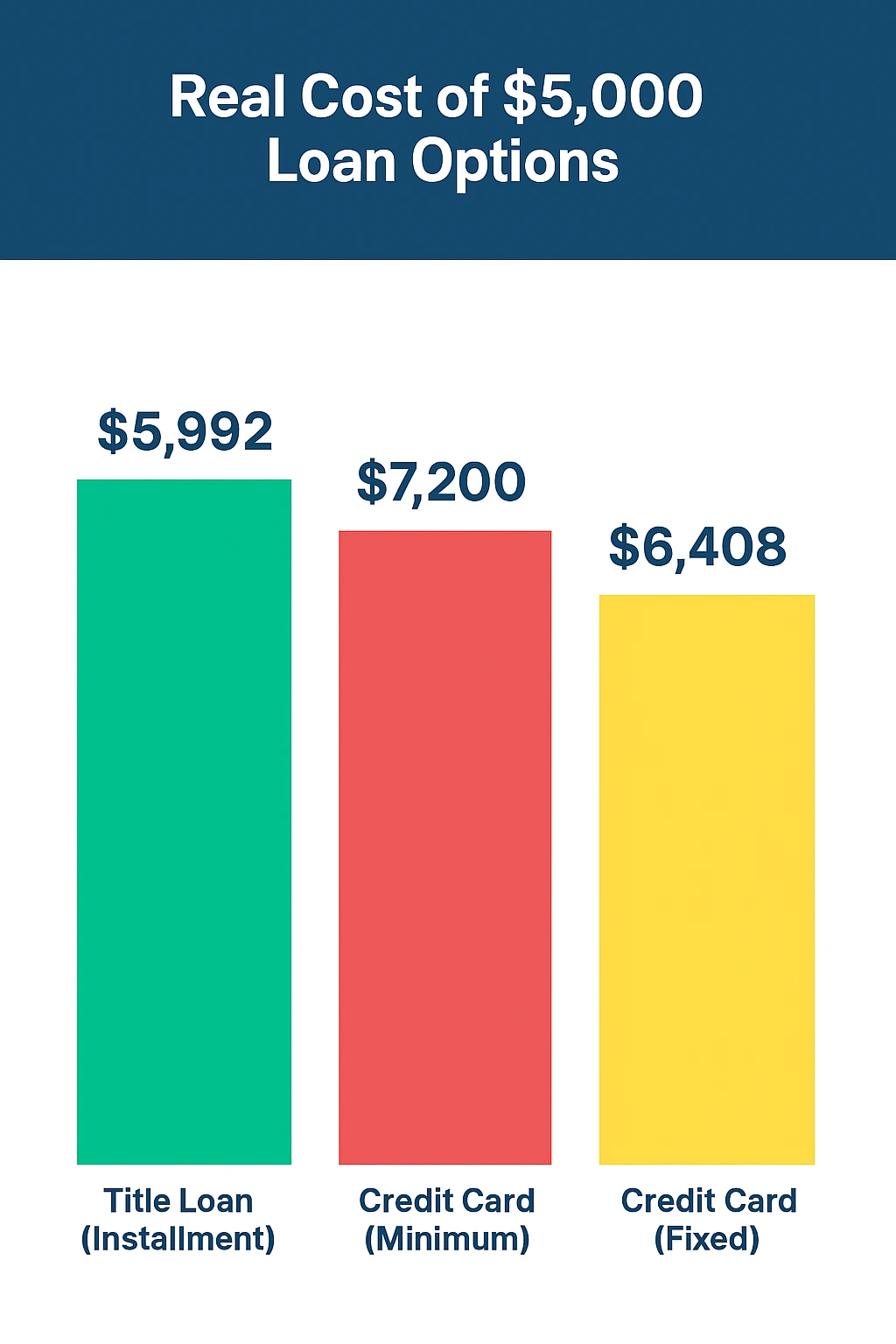

Real Cost Examples

Cost can change quickly depending on the loan amount, APR, fees, repayment term, and payment behavior. The example below is only an illustration. It is not a quote, approval, or guarantee.

$5,000 Cost Comparison Example

| Credit Type | Monthly Payment | Time to Pay Off | Total Interest Paid | Total Cost |

| Installment loan example | $208 | 24 months | $992 | $5,992 |

| Revolving credit, minimum payment example | $150 minimum | 48 months | $2,200 | $7,200 |

| Revolving credit, fixed $208 payment example | $208 | 26 months | $1,408 | $6,408 |

Example only. Actual rates, fees, payment amounts, and repayment terms vary by lender, borrower qualifications, state rules, and account terms.

Click image to view full size

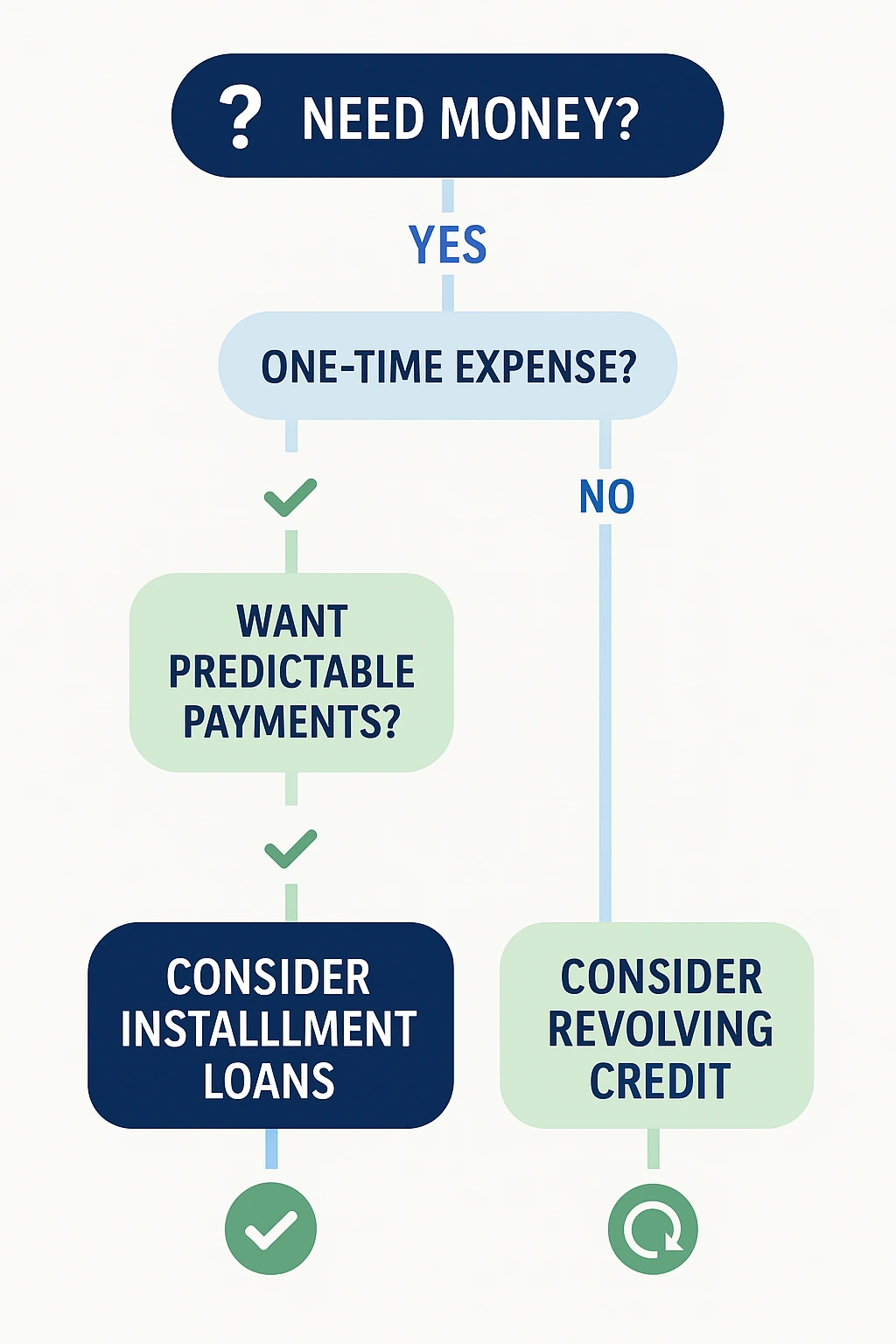

Which Option Is Right for You?

Start with the expense itself. A fixed, one-time cost usually points toward installment credit. Ongoing or uncertain expenses may fit revolving credit better, as long as you have a plan to keep the balance under control.

Consider an installment loan when you:

- Need a specific amount for a one-time expense

- Want predictable payments

- Prefer a defined payoff timeline

- Have a clear plan for how the funds will be used

- Want to avoid an open-ended balance

Consider revolving credit when you:

- Need ongoing access to funds

- Can pay more than the minimum payment

- Want flexibility for changing expenses

- Can keep utilization low

- Have steady cash flow to manage variable payments

Simple Borrowing Examples

One-time expense

A borrower needs a fixed amount for a repair bill and wants to know the payment schedule before signing. Installment credit may be easier to budget because the payment plan and expected payoff date are defined upfront.

Ongoing expenses

A borrower has smaller recurring costs and wants access to funds over time. Revolving credit may offer more flexibility, but the balance can become expensive if only minimum payments are made.

Installment Loans with Freedom Title Loans

Freedom Title Loans offers local title and installment lending options for Idaho borrowers. If you own a paid-off vehicle and need a set amount for a short-term expense, an installment-style loan may be worth comparing with revolving credit.

Start online, by phone, or at one of our Boise or Nampa branches.

Review repayment details before signing so you understand the schedule and cost.

Work with a Treasure Valley lender that serves Boise, Nampa, and nearby Idaho communities.

With a title loan, you can keep using your vehicle while repaying the loan, as long as the loan terms are met.

To compare local options, visit our installment loans in Idaho page or explore Freedom Title Loans locations in Boise and Nampa.

Making Your Decision

Before choosing between installment credit and revolving credit, answer these questions in writing. A short pause here can help you avoid borrowing more than you need.

- Do I need a set amount? If yes, installment credit may be the cleaner fit.

- Do I need ongoing access? If yes, revolving credit may offer more flexibility.

- Can I handle changing payments? If no, fixed payments may be easier to manage.

- Will I pay more than the minimum? If no, revolving credit can stay open longer and cost more.

- Do I understand the total cost? If no, ask for the full repayment details before signing.

Click image to view full size

Common Questions About Installment Loans and Revolving Credit

Is an installment loan the same as revolving credit?

No. An installment loan gives you one loan amount that you repay over a set term. Revolving credit gives you a credit limit that you can borrow from, repay, and use again.

Which is better for predictable payments?

Installment loans are usually better for predictable payments because the payment schedule is set at the start. Revolving credit payments can change based on the balance and interest charges.

Why can revolving credit cost more over time?

Revolving credit can cost more when a borrower carries a balance and makes only minimum payments. The balance can stay open longer, which can increase total interest.

Does revolving credit affect credit differently than installment loans?

It can. Revolving credit often affects credit through credit utilization, while installment loans are usually more tied to payment history, remaining balance, and account status. Reporting rules vary by lender.

Can a title loan be an installment loan?

Yes, some title loans are structured with scheduled payments over a defined term. The vehicle title is used as collateral, and the borrower keeps driving the vehicle as long as the loan terms are met.

Need help comparing options?

Talk with Freedom Title Loans Today

If an installment-style loan sounds like the better fit for your situation, we can walk you through local options in Boise and Nampa. We’ll explain the terms clearly so you can decide what works for your budget.